Given all of the data breaches in 2018 (Marriott Starwood, 1-800-FLOWERS, Quora, Walgreens, the Post Office, etc.) it is no longer a question of whether your data has been breached – you need to assume that it has been – rather the question is what is the best way to monitor your bank accounts and credit card accounts for fraudulent activity? And what are some non-obvious, technology-based ways to protect against it in the future? (The answer to the latter may surprise you!)

- In case you missed any of the above data breaches, most of which happened within the past 6 months, here are the links to the details about each one:

- 1-800-FLOWERS data breach

- Marriott Starwood data breach

- Quora data breach

- U.S. Postal Service data breach

- Walgreen’s data breach

So, assuming that your credit card and banking details have been compromised (which you should), what is the best way to monitor for any fraudulent activity? And what are some ways to guard against it in the future?

The Best Way to Monitor for Fraudulent Activity in Your Credit Card and Bank Accounts

The best way to monitor for fraudulent activity in your bank and credit card accounts is the same way – with a caveat – that the majority of data breaches happen: online.

By online we mean both through web-based banking and credit card account portals, and via smart-phone apps.

The Internet Patrol is completely free, and reader-supported. Your tips via CashApp, Venmo, or Paypal are appreciated! Receipts will come from ISIPP.

CashApp us

Venmo us

Paypal us

By caveat we mean assuming that you only log into your bank or credit card account via a secure connection, and that you use a strong password (and two-factor authentication if available).

Better yet, though, is if your bank or credit card provider has an app, through which you can access your account directly to review transactions, use that. Using your phone carrier’s data network (which, while not unhackable, is not as readily hacked as a wifi network) along with the security built in to today’s banking and credit account apps provides you with a measure of security while you are looking at your banking details.

Either method is far superior to reviewing your paper statements, or your emailed statements, although of course you can do that as well. But those only come out once a month, and a bad guy can do a whole lot of financial damage to you in a month.

And that last is why we recommend that you review your banking and credit card activity at minimum once a week, although several times a week is better. In fact, we monitor our primary accounts once a day.

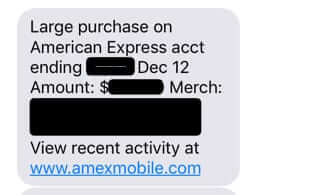

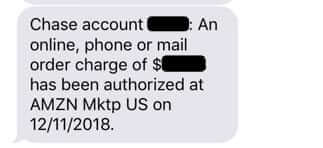

In addition, sign up for email or text alerts of charges to your accounts with every provider that offers them. For example, American Express and Chase both offer text message alerts of each and every charge transaction.

American Express and Chase Bank Notifications of New Charges

To recap, monitor all of your bank and credit card accounts, at least once a week, use phone apps offered by your financial institutions wherever possible, and sign up for text or email alerts of account activity if your credit card company and banks offer them.

Of course, if you see any activity that you don’t recognize, let your bank or credit card company know ASAP. The sooner you challenge a given charge, the easier it will be for your financial institution to reverse those charges, which they usually will with minimum hassle.

Speaking of, some will tell you that a credit card offers more protection against fraudulent activities than will a debit card. However, that is completely dependant on the individual institution. For example, here is what our bank said when we asked them about it:

Both types of cards are backed by VISA and by us as well so if you are ever a victim of fraud you would get a credit back into your account until research is complete; In both cases you would have to initiate the dispute by reaching out to the merchant first, if no success then completing the debit/credit card dispute form online.

In other words, this bank treats fraudulent charges to either a credit card issued by them or a debit card issued by them the same way. So if you use a debit card check, with your bank to see whether they reimburse for fraudulent activity in exactly the same fashion as they do a credit card.

Now, try to be as sure as possible that a transaction is actually fraudulent before reporting it – it will save you the hassle of your card having to be re-issued, and also the hassle to the legitimate merchant who charged you. A good example of this is the phone number 402-935-7733 that keeps showing up – unrecognized – on lots of people’s statements. It is actually Paypal, and the number can show up on your credit card statement when you either pay something through Paypal or when a merchant with whom you do business processes your credit card payment through Paypal. As you can tell by the over 1,000,000 readers who have read our article on why the number 402-935-7733 may be on your statement, a whole lot of people are consternated by that number appearing on their statement!

How to Protect Your Credit Cards and Bank Account Details Against Future Breaches

Believe it or not, your smartphone is also a key to providing more protection to your bank and credit card data in future breaches.

Using your phone’s ‘wallet’ enables you to pay with any credit or debit card you connect, without having the card with you at all. Not handing someone your actual credit card means the number can’t be grabbed. Smartphone wallets use near-field communication (NFC) to transmit your card info directly to the merchant without it ever being exposed.

Credit Cards in a Smartphone Wallet

Also, if your bank or credit card company offers virtual credit card numbers be sure to take advantage of it! These are one-use card numbers linked to your account, so you can give one of the virtual card numbers to a merchant, and if their data is breached it won’t matter because it won’t work anywhere other than that merchant.

Of course, the best way to make sure that your credit card data isn’t stolen and used fraudulently is to not use a credit card at all. But in this day and age that is increasingly difficult, if not downright impossible.

The Internet Patrol is completely free, and reader-supported. Your tips via CashApp, Venmo, or Paypal are appreciated! Receipts will come from ISIPP.

CashApp us

Venmo us

Paypal us